How Does Paying Off Only The Interest of Your Mortgage Affect Your Credit Score?

Topic

- Around India with MoneyTap 1

- Consumer Durable 1

- Credit Cards 32

- Credit Score 27

- Finance 33

- General 52

- Know MoneyTap Better 26

- MoneyTap 50

- MoneyTap in Daily Life 38

- Personal Loan 86

- Shopping on EMI 4

- Wedding Loan 1

Paying off a mortgage is an important milestone for a borrower. It is a step towards financial freedom. It is also a step towards bettering your credit score and thereby, your financial options. People resort to various means to pay off their debt, a common one being paying off only the interest. In fact, most believe that irrespective of how it is done, paying off a mortgage is sure to improve their credit score. To their surprise and dismay, this may not always be the case. Instances have occurred where borrowers paid off the mortgage and their credit score went down. The “how” of mortgage repayments has a significant impact on your credit rating. That’s why you must work out the best approach to repay your mortgage debt.

How do Mortgage Payoffs Work?

A mortgage comprises of the principal amount (the amount borrowed) and the interest incurred. Every mortgage typically has a minimum repayment threshold which applies first towards the interest and then towards the principal. For most mortgages, the law mandates that the minimum payment must be high enough so that it does pay off some of the principal balance. Banks do this to minimise their risk, to ensure that the debt is eventually paid off in a reasonable time frame.

How Does Mortgage Affect Your Credit Score?

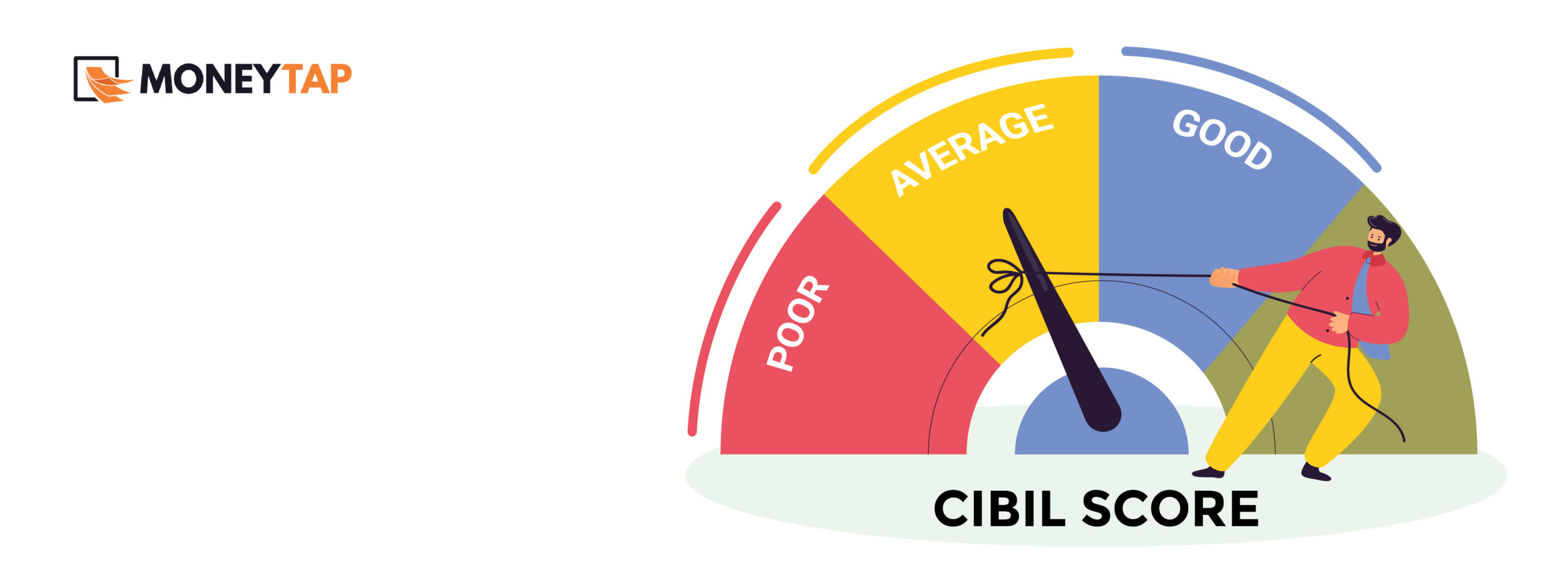

Mortgage debt and credit score follow an inverse relationship. The higher the credit score, the lower is the interest rate on the mortgage. This means that borrowers with high credit scores benefit, by generally availing lower interest rates on mortgages. Typically, a credit score (CIBIL Score) of 740+ should qualify the borrower for a mortgage.

How Mortgage Payoff Relates to Credit Score?

Paying off a mortgage loan in itself will not improve a borrower’s credit score. Also, when a borrower pays only the interest, the credit score may not decrease, but it will not also improve. This is because a borrower paying off only the interest leads to the principal amount remaining intact i.e. it remains the same as it was when the borrower first took the loan. This will result in a higher debt-to-income ratio. In effect, the credit rating system sees that the amount of available credit versus the current principal balance is the same. In effect, such as borrower is not paying back the mortgage to the extent he or she should. It is similar to having a fully utilised credit card (Link to: ) – not a great thing for a good credit score.

How to Improve Credit Score Despite Having a Mortgage?

A borrower can tackle this issue of mortgage repayments versus credit score, through two simple approaches. The first is to prepay the loan. The advantage here is that with prepayment, generally, you pay off the principal amount so that the loan tenure gets reduced and you end up paying less interest over time. Paying off the principal amount is an easy way to reduce loan outstanding and thereby increase the credit score. However, this may not be possible for everyone due to financial commitments. The alternative solution is to avail something called an interest-only mortgage loan.

Interest-only Mortgage Loan

Some banks such as SBI have introduced a new mortgage or home loan scheme where the borrower needs to pay only the interest component in the early years, generally for a period of five to seven years. Such a scheme with interest-only EMI can help the borrower avail greater loan amount. It is known to increase loan eligibility of the borrower by 20%. The risk is higher here and therefore there is a regularity mandate. Borrowers have to ensure cash resources they meet 10-20% of the property value through cash resources.

To avoid the hassle of low credit score and to secure financial security most people find it best to prepay their outstanding mortgage.

Nov 04

Shiv Nanda is a financial analyst at MoneyTap who loves to write on various financial topics online. He also advises people on financial planning, investment choices and budgeting skills, and helps them make their financial lives better.

Experience MoneyTap Power

Apply now

Subscribe Now

Topic

- Around India with MoneyTap 1

- Consumer Durable 1

- Credit Cards 32

- Credit Score 27

- Finance 33

- General 52

- Know MoneyTap Better 26

- MoneyTap 50

- MoneyTap in Daily Life 38

- Personal Loan 86

- Shopping on EMI 4

- Wedding Loan 1

Get it on playstore

Get it on playstore Get it on appstore

Get it on appstore