Can Banks Reject Personal Loan Applications When Credit Score is Above 800?

Topic

- Around India with MoneyTap 1

- Consumer Durable 1

- Credit Cards 32

- Credit Score 27

- Finance 33

- General 52

- Know MoneyTap Better 26

- MoneyTap 50

- MoneyTap in Daily Life 38

- Personal Loan 86

- Shopping on EMI 4

- Wedding Loan 1

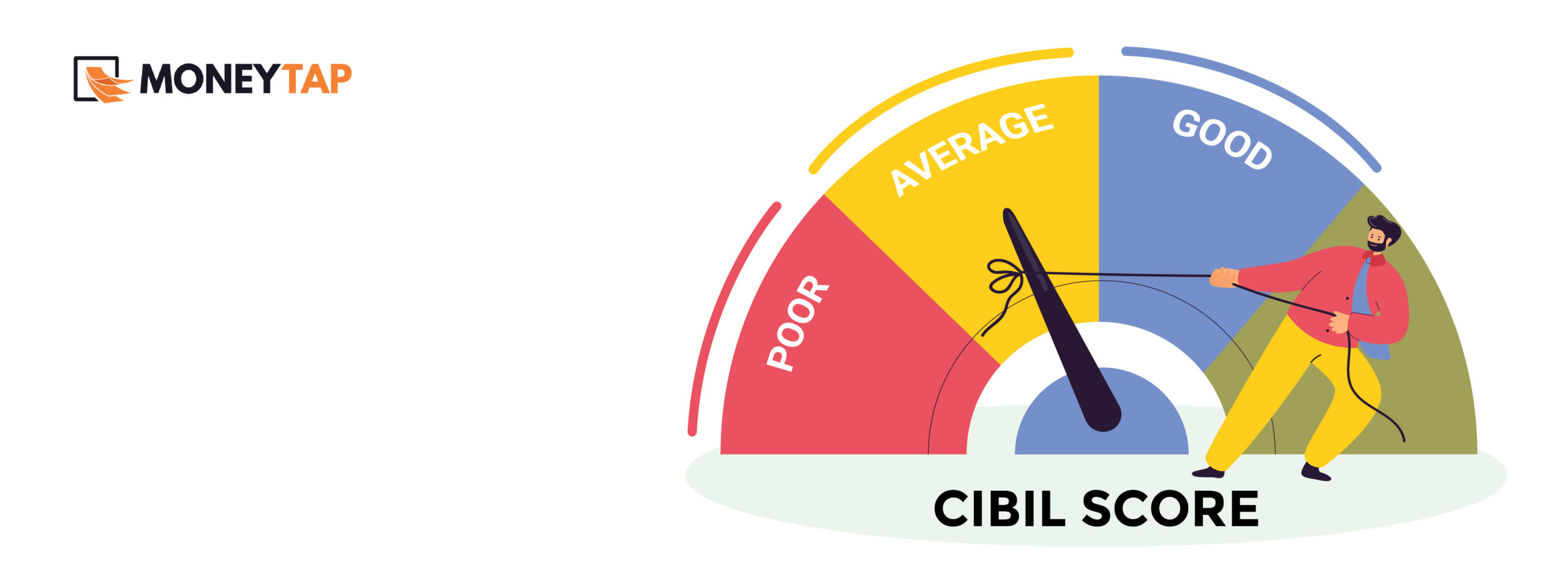

Applying for a loan at a bank can be a daunting experience; there is a lot of uncertainty about whether the loan will be approved or not. Most people are advised to work towards improving their credit score by making timely payments and not having too many ongoing loans parallely. Despite a good score, sometimes banks reject personal loan applications. In fact, a mere 79% of loans are approved for individuals with a CIBIL Score greater than 750. Here’s why this happens.

What is an Ideal CIBIL Score?

CIBIL score varies in the range of 300 to 900, with anything above 700 being considered a decent score. Anything above 750 is considered a good credit score for loan approval. However, it is a myth that you are guaranteed a loan if your credit score is above 800. This places a lot of inconvenience on the loan applicant, he or she can never be sure of availing a loan even for basic life needs like home, wedding etc.

Loan Rejection Reasons

The uncertainty in loan allocation stems from the fact that banks do not look at only the numeric Credit Score to carry out loan decisions. They also evaluate the following:

- Defaulter Details: Every bank maintains a database of defaulters, and checks the loan applicant’s details against this list. If it finds a match, it will reject the loan application irrespective of the CIBIL score.

- Comments: The CIBIL report contains comments and remarks by previous lenders. These outline how the applicant settled prior loans. For example, if the loan was settled in an unconventional manner (for example an interest rate reduction), it will work against the applicant. Other comments that can make getting a loan difficult are “settlements”, “written off loans”, or loans paid after the due date.

- Being a Guarantor on a Default Loan: Most loans require a guarantor to be allocated. If the applicant was a guarantor on a defaulted loan, it adversely affects the chances of loan allocation.

- Overleverage: A borrower can assign only a certain part of his or her income to debt instruments. Hence a high number of outstanding loans at the same time above this threshold can get your personal loan application rejected. For this, banks study the applicant’s debt-to-income ratio.

- Too Much Borrowing: Banks analyse the previous years’ loan borrowing, irrespective of whether they have been paid back or not. If a borrower is found to borrow too frequently, the loan may be rejected because he or she is deemed credit-hungry. Such a candidate is considered risky.

- Secured Versus Unsecured Loans: The nature of loans one avails i.e. secured versus unsecured is an important consideration for banks to allocate further loans. More number and amount of unsecured loans poses a grave risk to banks. Ideally, the applicant must have more number of secured loans than unsecured loans.

- Default on Tax Payments: An applicant who has not regularly filed income tax for the past two years is at risk of loan rejection.

Anyone who wants to secure a loan must, therefore, work towards improving the above factors, apart from the CIBIL score itself. This is how you can do it:

How to Improve Your CIBIL Score?

- Correct Inappropriate Information: Sometimes the information such as personal details, active credit cards etc. may reflect incorrectly in your Credit Information Report. This may lower your credit score, hence you must address it and get it corrected on priority by reporting the same to CIBIL and the concerned bank or financial institution.

- Pay Off All Credit Cards: Even if you are paying the minimum due on your credit cards, it means that you are availing an ongoing loan. It is advisable to clear off all credit card dues before the due date, and not just the minimum outstanding.

- Hold on to Old Credit Cards: Building a good repayment history over a long period of time is a great way to up your credit score. Therefore, rather than discarding old credit cards, retain them and use them as a preference for newer credit cards.

- Maintain Credit Utilisation: Just because you are entitled to 1 lakh of revolving credit through your credit card does not mean you utilise it all. Maintain a habit of 30% credit utilisation, and you will see your credit score soaring.

- Seek Credit Limit Enhancement: From time to time, banks offer a reliable customer the option to enhance their credit limit. Opt for it, because it is an indication of timely payments and good credit worthiness and can help increase your credit rating. Of course, you should not utilise that enhanced limit.

- Seek Alternative Lending Sources: Look for alternative options like peer to peer lending to diversify your credit history. Many of these loans, like MoneyTap, offer credit very quickly and at affordable rates, making them easy to pay back. This can prove a boon to your credit history.

Nov 04

Shiv Nanda is a financial analyst at MoneyTap who loves to write on various financial topics online. He also advises people on financial planning, investment choices and budgeting skills, and helps them make their financial lives better.

Experience MoneyTap Power

Apply now

Subscribe Now

Topic

- Around India with MoneyTap 1

- Consumer Durable 1

- Credit Cards 32

- Credit Score 27

- Finance 33

- General 52

- Know MoneyTap Better 26

- MoneyTap 50

- MoneyTap in Daily Life 38

- Personal Loan 86

- Shopping on EMI 4

- Wedding Loan 1

Get it on playstore

Get it on playstore Get it on appstore

Get it on appstore